FoodExpoConnect Blog

SeriesUS–China Trade Reset 2026Global Food Trade Tariffs in 2026: How US-China-EU Trade Tensions Are Reshaping Agricultural Exports

US baseline 10% tariffs with up to 50% country-specific rates are restructuring global food trade. Brazil, Canada, and India face steep rates. Here's how food exporters can navigate the new tariff landscape.

The global food trade is navigating its most disrupted tariff landscape in a generation. The US baseline tariff of 10% on goods imports — with country-specific reciprocal rates climbing to 50% — has triggered a cascade of retaliatory measures, trade diversion, and market restructuring that reaches every corner of the agricultural export industry.

For food exporters in Africa, Asia, and Latin America, the tariff war creates both existential threats and unprecedented opportunities. Understanding which doors are closing and which are opening is the difference between losing your biggest market and finding a better one.

The Tariff Landscape: May 2026

The numbers are stark. A Cornell-Ohio State University study published in April 2026 found that the US tariff regime has imposed measurable economic costs on all 50 American states — not just the agricultural heartland, but every state through higher food prices, disrupted supply chains, and lost export markets.

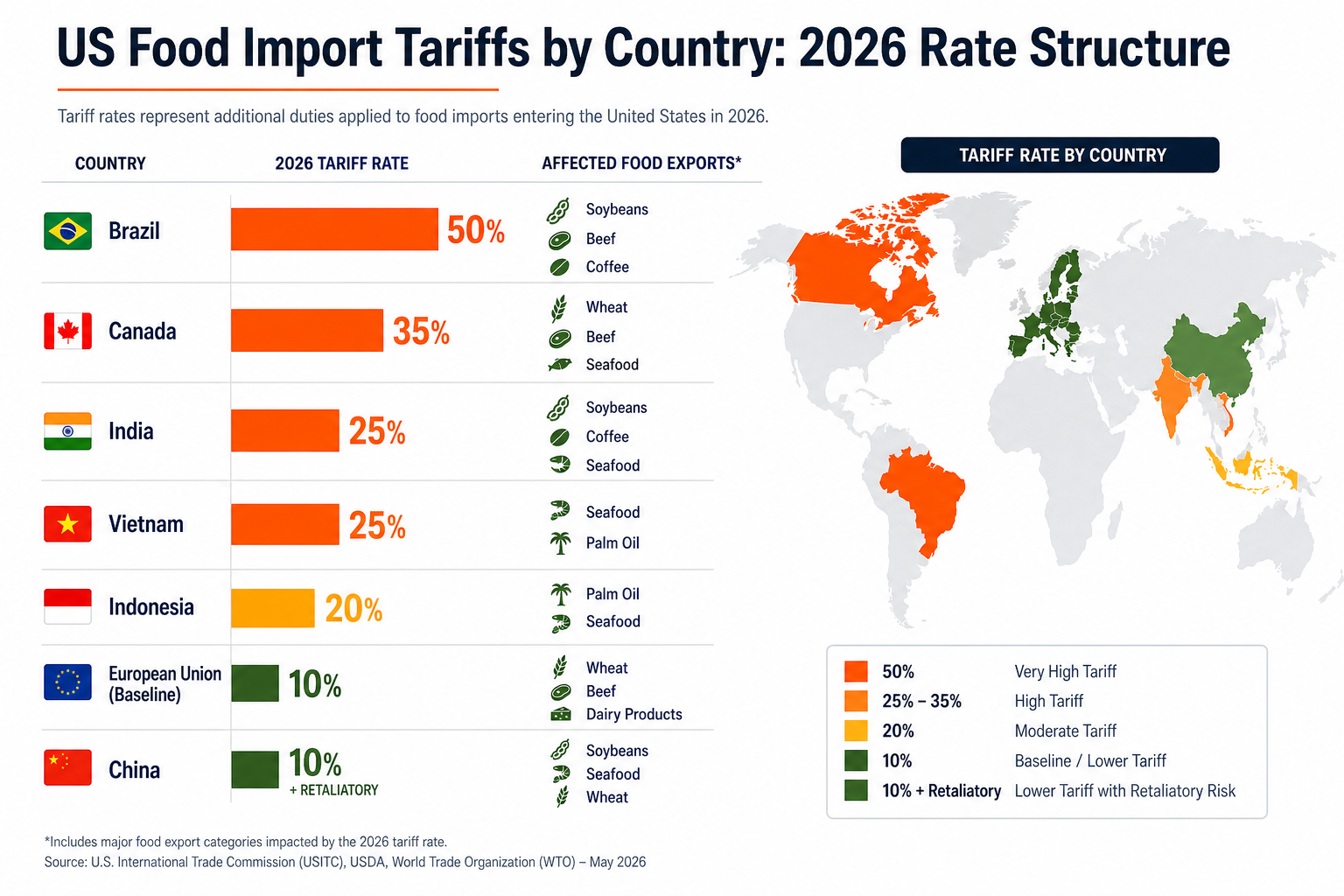

| Country | US tariff rate | Key affected exports |

|---|---|---|

| Brazil | 50% | Soybeans, beef, coffee, orange juice, sugar |

| Canada | 35% | Wheat, canola, pork, beef, dairy |

| India | 25% | Rice, spices, shrimp, processed foods |

| Vietnam | 25% | Coffee, seafood, cashews, pepper |

| Indonesia | 20% | Palm oil, coffee, cocoa, spices |

| EU (baseline) | 10% | Wine, cheese, olive oil, processed foods |

| China | 10% + retaliatory | Soybeans, pork, corn, wheat, beef |

The framework agreements negotiated between April and August 2025 provided some relief — countries that agreed to provide market access for US goods received lower tariff rates. But the baseline structure remains, and the retaliation cycle continues.

The China Factor: Soybeans, Pork, and the Great Diversion

China's retaliatory tariffs on US agricultural products have reshaped global protein and grain markets. US soybean exports to China — which reached $14 billion at their peak — have declined by an estimated 40-50%. China has replaced US soybeans primarily with Brazilian and Argentinian supply.

The Brazilian soybean industry has been the single biggest beneficiary. Brazil's share of Chinese soybean imports has risen from roughly 60% pre-tariff to an estimated 75-80%. Brazilian soybean farmers have expanded planted area by an estimated 8-12% since the tariff escalation began, largely in the Cerrado region.

But the Brazil-China soybean corridor is not without risks. Chinese buyers, aware of their concentrated sourcing, are actively seeking additional diversification — creating opportunities for African and Southeast Asian soy exporters who can meet quality specifications.

The soybean lesson for food exporters: when the world's largest buyer is forced to restructure its supply chain, the second-order effects ripple for years. The exporters who positioned themselves as alternative suppliers in 2025-2026 will have established buyer relationships that persist long after the tariff dispute is resolved — if it ever is.

The Canada-US Food Trade Shock

The 35% reciprocal tariff on Canadian agricultural exports has been particularly disruptive because of the deep integration of US-Canada food supply chains. Canadian pork, beef, wheat, and canola have flowed across the border for decades under NAFTA/USMCA frameworks that made cross-border trade nearly frictionless.

The impact runs both directions. American farmers face higher costs for Canadian potash fertiliser — a critical input for corn and soybean production. Canadian food processors who relied on the US market for 60-70% of their sales are scrambling to find alternative buyers. And consumer prices for food products that cross the border multiple times during processing — a common feature of the integrated North American food system — have risen 8-15%.

For exporters outside North America, the US-Canada tariff shock creates a specific opportunity: replacing Canadian supply in the US market. Mexican and Central American beef exporters, Australian and New Zealand dairy exporters, and EU pork exporters are all competing for market share that Canadian producers are being priced out of.

The EU-US Agricultural Trade Standoff

The EU-US agricultural trade relationship is asymmetric: the US imports nearly three times more agricultural products from the EU ($44 billion in 2023) than the EU imports from the US. EU wine, cheese, olive oil, and processed foods dominate American supermarket shelves.

A framework agreement between the EU and US could open American agricultural exports to the European market — a significant prize for US farmers. But negotiations are stalled on two issues: the EU's system of geographical indications (which prevents US producers from using names like "Parmesan" or "Champagne") and food safety standards (the EU prohibits chlorine-washed chicken and hormone-treated beef that are standard in US production).

For food exporters in Africa, Asia, and Latin America, the EU-US standoff is a mixed signal. A deal would increase US competition in the EU market. No deal preserves the status quo — but the status quo includes 10% US tariffs on EU food imports, which are already reshaping sourcing decisions.

Winners and Losers: The Global Reshuffling

Who Is Winning

Brazil: The clearest winner. Brazilian agriculture has captured market share in China (soybeans, corn, beef), the EU (soybeans, coffee), and the Middle East (poultry, sugar). Brazilian agricultural exports reached record levels in 2025, driven largely by trade diversion from tariff-affected competitors.

Australia: Australian wheat, beef, and wine have benefited from reduced US and Canadian competition in Asian markets. Australian wheat exports to Southeast Asia increased 18% as US wheat became less competitive due to shipping costs and trade uncertainty.

Vietnam: Vietnamese coffee, seafood, and cashew exporters have gained from reduced competition in both the US and Chinese markets. Vietnam's processed food sector — particularly instant coffee and packaged seafood — has expanded rapidly as buyers seek alternatives to tariff-exposed suppliers.

Turkey and Morocco: These Mediterranean-adjacent food exporters have seen European buyer interest increase 20-30% as European importers reduce exposure to tariff-uncertain and Red Sea-disrupted origins.

Who Is Losing

American Farmers: A study by the American Enterprise Institute found that US agricultural exports declined approximately 12-15% in value terms in the first year following tariff implementation. Soybean farmers in the Midwest, pork producers in Iowa, and corn farmers across the Corn Belt have been particularly affected. Government support payments have partially offset losses but do not replace lost market access.

Canadian Food Exporters: The 35% tariff rate has made Canadian pork, beef, and wheat significantly less competitive in their largest market. Canadian food exporters are investing heavily in market diversification — targeting Japan, South Korea, the EU, and Southeast Asia — but replacing the US market at scale takes years.

Food-Importing Developing Nations: Countries that depend on imported staple foods — wheat, corn, rice, vegetable oil — face significantly higher prices as global trade flows are disrupted. The World Food Programme has reported that its food procurement costs have increased 12-18% since the tariff escalation, directly reducing the number of people it can feed with the same budget.

The Opportunity for African and Emerging-Market Food Exporters

For food exporters in Africa, South Asia, and Latin America who are not subject to high US tariff rates, the tariff war creates a strategic window. Here's what's opening:

1. US Market Access for Non-Tariffed Origins

If you export from a country with the baseline 10% US tariff rate (or lower, if negotiated through a framework agreement), you have a 25-40% price advantage over Brazilian and Canadian competitors in the US market. A Ghanaian cocoa processor, a Kenyan coffee exporter, or a Peruvian fruit exporter can price 15-25% below a Brazilian equivalent and still maintain healthy margins.

2. Chinese Supply Chain Diversification

Chinese food importers — burned by their over-reliance on US and Brazilian supply — are actively seeking third-country suppliers. The China-Africa agricultural trade corridor, in particular, has seen accelerated investment. Chinese state-owned food companies have opened procurement offices in Ethiopia, Tanzania, and Mozambique, seeking soybeans, sesame, coffee, and cashews.

3. EU Market Stability

While the EU-US tariff dynamic affects wine, cheese, and processed foods, the EU's import demand for tropical commodities (coffee, cocoa, spices, tropical fruits) is largely tariff-insulated. For most developing-country food exporters, EU market access has not materially changed — and may have improved if your competitors have diverted product to tariff-affected US and Chinese markets.

4. Regional Trade Bloc Acceleration

The tariff war is accelerating the implementation of regional free trade agreements. The African Continental Free Trade Area (AfCFTA), the Regional Comprehensive Economic Partnership (RCEP) in Asia, and the EU's Economic Partnership Agreements with African, Caribbean, and Pacific states are all seeing accelerated utilisation as exporters seek tariff-free alternatives to disrupted US and Chinese markets.

Practical Strategy for Food Exporters

Audit Your Tariff Exposure

Map every export destination against current tariff rates. A product that was profitable at 0-5% tariff may be unprofitable at 25%. A product that was uncompetitive at 15% tariff may suddenly be competitive when your competitors face a 35-50% rate. The tariff landscape has shifted the competitive calculus — recalculate it.

Diversify Buyer Geography

If more than 60% of your exports go to a single market — especially the US or China — the tariff war is an existential concentration risk. Even if you're not currently affected, the next round of tariff adjustments could hit your category. Build buyer relationships in at least two additional geographic markets.

Leverage Trade Agreements

Every major importing bloc has preferential trade agreements with developing countries. The EU's Everything But Arms (EBA) initiative, the US African Growth and Opportunity Act (AGOA), China's duty-free access for Least Developed Countries — these programmes often provide zero-tariff access that insulates you from the broader tariff war. If you're not using them, you're leaving money on the table.

Watch the Currency Dimension

Tariffs don't exist in a vacuum. The US dollar has strengthened against most emerging-market currencies since the tariff escalation, making US imports more expensive in local-currency terms and US exports less competitive. For food exporters earning in dollars and paying costs in local currency, this is a tailwind. For importers of US food products, it's a headwind on top of the tariff.

Build Compliance Into Pricing

US customs enforcement has tightened significantly. Misclassification of products to avoid tariffs carries severe penalties — fines, shipment seizure, and in some cases, criminal liability for knowing violations. If your product faces a high tariff rate, factor it into your pricing and compete on quality and reliability, not tariff avoidance.

Looking Ahead: Scenarios for 2027

Negotiated settlement (30% probability): The US negotiates framework agreements with most major trading partners, reducing the highest tariff rates to 15-25%. Agricultural trade partially normalises, but the supply chain restructuring of 2025-2026 leaves permanent changes in sourcing patterns.

Prolonged standoff (50% probability): The baseline tariff structure remains through 2027. Supply chains continue to restructure around tariff barriers. Countries with preferential access (through trade agreements or low reciprocal rates) consolidate their market share gains.

Escalation (20% probability): A new round of tariff increases — possibly triggered by a specific trade dispute — pushes rates higher. Secondary sanctions or trade restrictions on food commodities (which have largely been avoided so far) could fundamentally alter global food availability and prices.

The 50% scenario is the one to build your business plan around. The tariff structure is durable enough to justify permanent supply chain changes, but not so extreme that it halts global food trade entirely.

Jean-Marc du Plessis is a food export strategist and MBA graduate of INSEAD with 14+ years of experience in African agricultural exports. He has facilitated over $9.5M in food export transactions across 18 countries and regularly advises exporters on trade policy compliance and market entry strategy.

Frequently asked questions

What are the current US tariff rates on food imports in 2026?

How have tariffs affected global food prices?

Has China retaliated with tariffs on US food exports?

Which countries benefit from the US-China food trade disruption?

What is the EU-US trade negotiation status for agriculture?

Quick facts

Published: 5/8/2026

Reading time: 12 min

Pillars: Global Trade, Tariffs

Written by

Jean Marc Koffi

Co-authorJournalist & Export SpecialistLondon

Jean Marc Koffi is an MBA-trained trade specialist who connects African exporters to global buyers, with over $20M in contracts facilitated and expertise recognized by major trade organizations. Noted for rapid buyer network building, he is an experienced speaker and certified in trade facilitation, origin rules, and food safety.

Alocha Massamba

Co-authorFounder, Epifresh & FoodExpoConnectLondon

Alocha Massamba is the founder of Epifresh and FoodExpoConnect. He builds the technology, data and partnerships that connect African food producers and exporters to international buyers — with a focus on fresh-produce supply chains, cold-chain logistics, and the buyer-discovery platforms small and mid-size exporters need to compete with global incumbents.

Series

More in US–China Trade Reset 2026

US-China Trade Deal May 2026: What the Trump-Xi Summit Means for African and Latin American Food Exporters

The Trump-Xi Beijing summit produced a commitment for China to buy 25 million metric tons of US soybeans annually through 2028 — and 'double-digit billions' in broader agricultural purchases. Here's what the reconfigured US-China food corridor means for exporters in Africa and Latin America.

US-China Trade Reset 2026: What the Trump-Xi Tariff Deal Means for Food Exporters Worldwide

The May 2026 Trump-Xi tariff reduction framework covering $30 billion in bilateral trade is reshaping global food export flows. African and Latin American exporters stand to gain as US soybeans and beef face continued uncertainty in Chinese markets.

Explore more export intelligence

Export Operations • Finance • Risk Management

Letter of Credit vs Documentary Collection: When to Use Each (2026 Decision Guide)

Letters of credit and documentary collections both reduce payment risk in food export — but the wrong choice costs you $200-500 per transaction in unnecessary bank fees. This decision guide with real scenarios shows exactly when each instrument makes sense.

Export Operations • Tools & Software • Food Manufacturing

Best ERP Software for Small Food Manufacturers in 2026: MRPeasy vs Odoo vs Katana Compared

Running a food manufacturing business on spreadsheets and sticky notes costs you 15–20% of production capacity in planning errors, inventory waste, and compliance failures. We compared the top four ERP systems built for small food manufacturers — here's which one actually fits your operation.

Export Strategy • Pricing & Profitability • African Exports

Pricing Premium for African Food Exports: How to Capture 25-40% Margin Uplift Through Premium Positioning (2026)

African food exporters routinely leave 25-40% margin on the table by selling commodity-grade. We break down the premium positioning strategies — certification, storytelling, packaging, and direct buyer relationships — that turn $4/kg cashews into $12/kg specialty product.